2023 Year Planner Is Out Now

22 December 2022

Setting KPIs and Measuring Performance

19 January 2023

When it comes to financial reporting, there are two main methods businesses can use: cash reporting and accrual reporting. The difference between these two methods lies in the timing of when income and expenses are recorded.

Why it's important

It's essential to have a clear understanding of how each financial reporting method works, even if you don't handle the reporting yourself. This way, you can choose the bookkeeping practices that best fit your business.

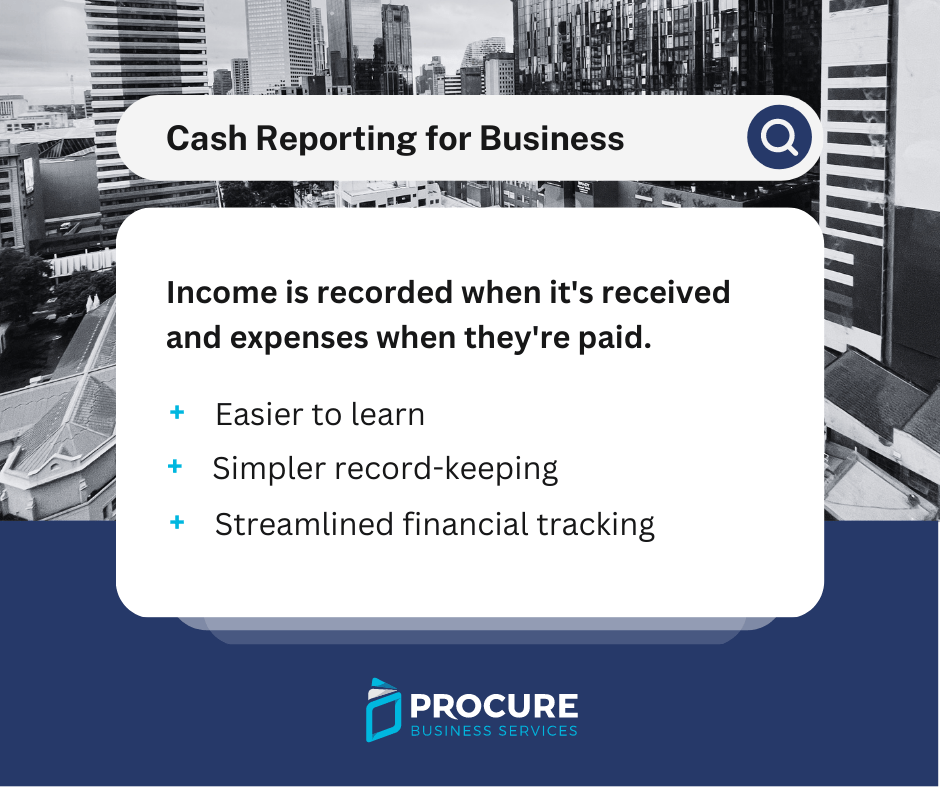

Cash Reporting

Income is recorded when cash is received in your bank account, and expenses are recorded when money is paid out of your bank account. In this method, income and expenses are reported in the financial period that the cash transaction occurred. This method is simpler and easier to manage for small businesses with a turnover of less than $10 million. However, it's not always as accurate as the accrual system.

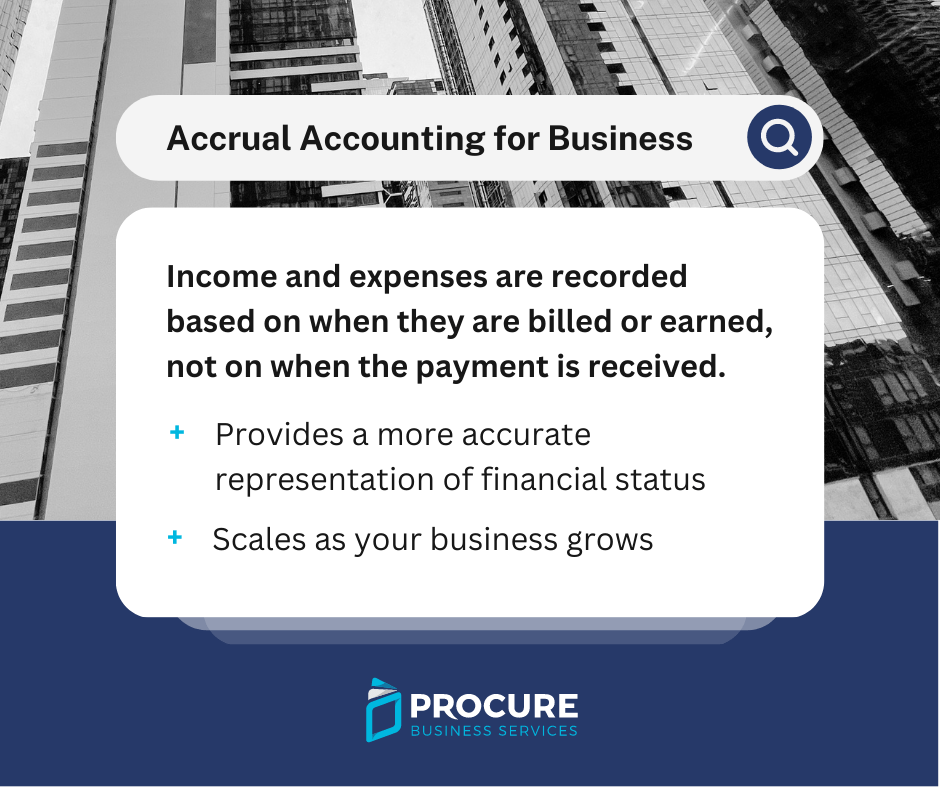

Accrual Reporting

Income is recorded when a customer is invoiced, and expenses are recorded when suppliers issue bills. In this method, income and expenses are reported in the financial period that the transaction was created, regardless of whether a payment was received or made. This method is more accurate for planning and decision-making and gives a longer-term view of a business's financial position.

BAS and Tax Returns

For the Business Activity Statement (BAS), many small businesses are registered for cash reporting. However, for income tax calculation, the tax agent generally reports on an accrual basis.

Choosing the right option for your business

In summary, while cash reporting is simpler and easier for short-term financial management, accrual reporting provides a more accurate picture for long-term planning and decision-making. If you're unsure about which method is best for your business, don't hesitate to book a 30-minute free consultation.

{kind=link}

{kind=link}